Digital money: utopian dream or totalitarian nightmare?

Almost 100 nations are developing their own centralised currency, sparking fears about rising totalitarianism – are we really one digital dollar away from living in an episode of Black Mirror? An expert weighs in

Digital money is at a turning point at the start of 2023, after a shaky 2022. In case you need a refresher: last year saw the Bitcoin market lose more than $2 trillion since the world’s most famous cryptocurrency peaked in value 12 months earlier, and FTX (the world’s second biggest crypto exchange) underwent a highly public crisis that exposed the wobbly foundations of even the industry’s biggest players.

On the other hand, cryptocurrencies continue to become increasingly legitimised: in El Salvador you can buy a Big Mac with Bitcoin, and increasing calls for regulation in the US and Europe reflect a begrudging acceptance that crypto is here to stay. A few months before he was elected the UK’s prime minister, Rishi Sunak even got the Royal Mint to make an NFT, signalling “the forward-looking approach we are determined to take towards crypto-assets”.

One of the biggest signs that physical cash could die out in our lifetimes, though, is that more than half of the world’s central banks – national banks that manage countries’ currency and monetary policy – are working on their own digital currency, according to the International Monetary Fund. These currencies are known as CBDCs (which, despite sounding like a famed NYC punk venue, stands for the much more boring term “central bank digital currencies”) and would allow transactions to be made near-instantaneously, and at negligible cost, across the world.

Turns out, some people aren’t particularly enthusiastic about the prospect of a digital currency controlled by central banks, though – and their fears aren’t unfounded. Over the last month, TikTok explainers and Twitter threads have popped up warning that CBDCs will be used by governments to usher in social credit systems, exert control over the population, and basically turn life into an episode of Black Mirror.

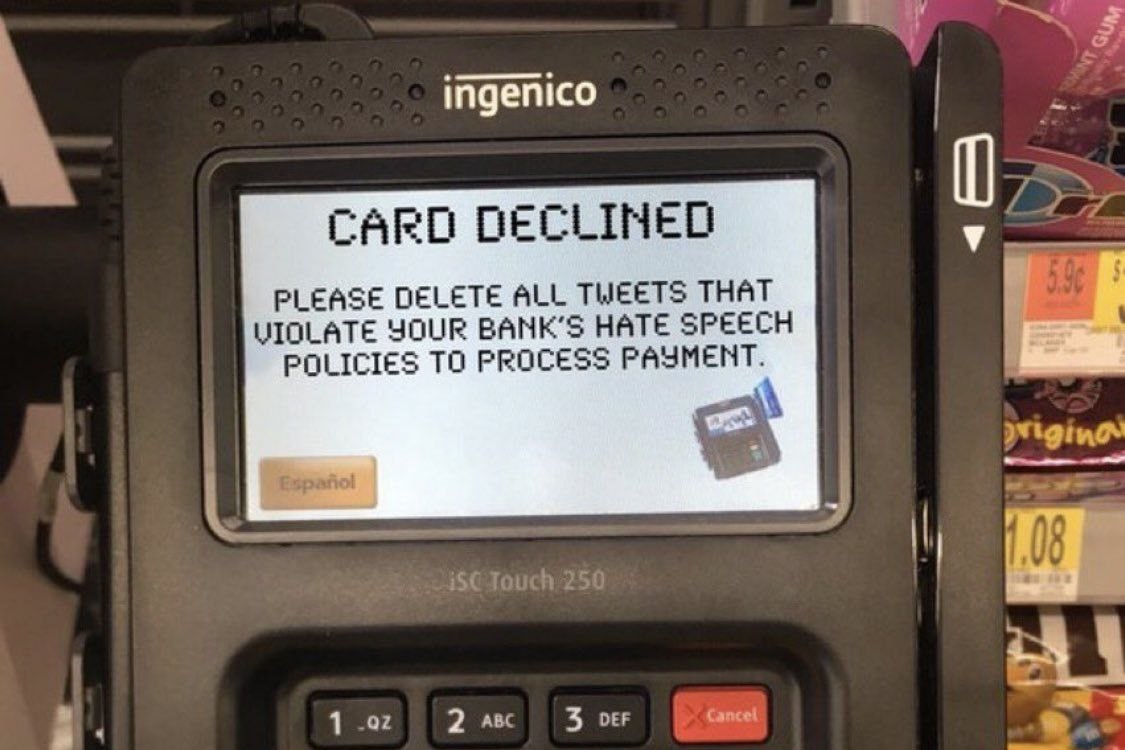

“Because the government would now have the power to track, delete and create money instantly, people are worried [it] could implement monetary policy that’s ‘good for the economy’ but terrible for you,” says one TikToker, in a video that’s been watched over two million times. A popular meme, meanwhile, shows a card reader displaying the message: “Card declined. Please delete all tweets that violate your bank’s hate speech policies to process payment.”

Do CBCDs actually pose a threat to our freedom, though, or is the current wave of panic just another case of conspiracy theorists fearmongering about any new technology that comes along? We spoke to Garrick Hileman, research associate at the University of Cambridge and London School of Economics, about what they could mean for us.

Why are we suddenly talking about CBDCs?

Garrick Hileman: The short answer is Bitcoin. Bitcoin prompted a discussion about the future of money and what it should look like, and whether or not governments and central banks needed to upgrade money. I think the general consensus after a decade of discussion, and five years of actual experimentation is: yes, money does need to be upgraded.

Why does it need to be upgraded? What’s wrong with the current system?

Garrick Hileman: Well, the problems that upgraded money could solve are quite significant, and represent a vast cost to society. This cost is actually invisible to the everyday person, but it’s very real. When you pay for food, or say a TV, with your credit card, there’s often a charge that credit card companies apply, that the merchant pays. You, the consumer, never see it, but believe me, that one-and-a-half, up to sometimes five per cent charge for spending money via credit card or debit card is absolutely embedded in the cost of everything you buy.

When you compare that cost to what it costs for us to have this call right now on Zoom, or sending a text message anywhere in the world, or sending an email… that’s all effectively free. [There’s] a huge difference between the cost of money and the cost of other forms of electronic communication, which is in essence what money is – it’s just an information network, [and] many think the cost should be free.

Then, there are speed problems. Getting money from A to B, especially internationally, can take days or weeks. Also, international money transfers can cost up to 20 per cent in sketchy conversion fees, particularly to emerging markets like Africa, and places with less developed financial infrastructure. In other words, the people who can least afford to pay a 10 to 20 per cent transaction fee often pay the highest fees to move money. It’s absolutely inexcusable, in 2023, that someone who’s struggling to put food on the table for their family in, say, Nigeria or Somaliland, has to spend 20 per cent to get the money they’re earning in London back home. It’s absolutely criminal. And it’s a problem the world’s known about for decades and has been unable to solve. CBDCs, or upgraded money, or cryptocurrency, are all efforts to finally try to solve this problem and make money more like sending a text message or an email – free and relatively instantaneous.

‘In 2023, someone who’s struggling to put food on the table for their family has to spend 20 per cent to get money they’re earning back home. It’s absolutely criminal’ – Garrick Hileman

How else could CBDCs affect our daily lives?

Garrick Hileman: It really depends now on how the CBDC is designed, and this is where the political implications start to come up. [At the moment] there are different approaches being pursued. China’s at one end of the spectrum, and you can think of Europe as kind of in the middle, and the US is at the other end of the spectrum, opposite China.

The US idea is to not do it at all. That’s where the United States and the Federal Reserve is at right now. Now, that’s not a universally held view. There are certain legislators and others who want to see a CBDC, and the Boston Federal Reserve has been piloting technology, but the chairman of the Fed and others have made it clear that there’s a stronger consensus around not doing anything at all.

The other end of the spectrum is China, which is a totally state-run panopticon surveillance nightmare that would make Orwell blush, frankly, with how invasive and all-powerful it is, when you pair it with a social credit score and other surveillance technology. China has basically developed [financial tech] to try to wrest back control of payments and money from the private sector and put it in the hands of the government, and give them that added power to censor transactions. If you’ve been at a COVID protest or something, you might not be able to access a loan. This would be another mechanism of control in a country like China, pursuing a very government-driven, zero-privacy CBDC.

Somewhere in the middle is Europe, although it’s still very early days there. It’s between doing nothing like the US, and total government control like China. I would argue the direction that the Eurozone seems to be leaning toward is closer to the Chinese approach than the US approach.

So people’s fears that CBDCs could be used to enforce a social credit system are kind of valid?

Garrick Hileman: I think people should be worried, yes. The power to monitor all of your financial transactions, to block your ability to make payments… we saw this happen with the Canadian trucker strike last year, where the Canadian government exercised emergency powers to block the financial transactions of those found out to be participating in those protests. That’s a very real example, in an advanced economy that’s the closest of allies [with the US and UK]. So, yeah, I think that’s a very real concern.

There are more subtle issues as well. There are Orwellian nightmare stories, but there are also seemingly little things. Many economists dream of the ability to implement what are called negative interest rates. Now, what is that? Basically, some economists would like to jumpstart spending in an economic downturn by actually making your money lose its value faster and faster, and forcing you to spend it. If you have cash, that doesn’t work, because people can pull cash out of a bank. But if you’re locked into a digital cash system you don’t have the option to take cash out. [Governments] could say, ‘OK, citizens, you need to start spending your money now or you’re going to lose 10 per cent.’ Economists will argue that’s great, because if we’re in a real economic downward spiral, we can force people to spend their money.

Essentially, if an idea benefits the overall economy but has a negative effect on individual citizens, it could be implemented without any barriers?

Garrick Hileman: Correct. I think the intentions are good – I’m not implying that there’s a sinister agenda here. But whenever you implement a broad policy, there are winners and losers, right? And those winners and losers oftentimes don’t have much political voice, when a technocrat is making a decision like that. They’re just caught up in the ripples of that decision.

“This is such an important technology that you cannot leave it to the technocrats to make all the decisions… there are major implications for individual privacy and financial access” – Garrick Hileman

Another fear is that CBDCs will allow governments to harvest unprecedented amounts of data, with details of every transaction a citizen makes. Is this a valid concern?

Garrick Hileman: Yeah, but let’s look at some of the upsides of this enhanced surveillance and tracking capability as well. The Queen came to the London School of Economics shortly after the 2008 Lehman failure and basically just dressed down a bunch of economists with what’s now known as the Queen’s Question. She asked them all: ‘Why didn’t any of you see this coming?’ And the reason is, number one, that the economy is constantly evolving and shifting, so your model that predicted what happened in the past doesn’t work for today’s economy. Number two, cause and effect is very difficult to disentangle. And then number three is [that] the quality of data is very poor.

Having more digital economic activity could be incredibly valuable for better data, and maybe improving our models, so we can have soft landings rather than a recession, or hopefully not a depression. That’s one benefit. The second benefit is that society doesn’t work if some people are paying their taxes and others aren’t. If you’re aware that your neighbour is getting away with not paying their taxes, why would you pay yours? Society breaks down unless you have a fair tax system, where everyone feels like people are paying their fair share. Digitising economic activity could potentially lead to a more equitable, balanced and compliant tax collection regime.

Does that include more transparency about how we tax corporations and the hyper-rich?

Garrick Hileman: Absolutely. The whole scandal around VAT in Europe, and all the games that get played there, that’s a huge issue. This is actually, I think, one of the most exciting things about digitising finances: you could automate a lot of tax collection, so there isn’t even the option to cheat.

“I’ve heard regulators say: ‘Well, why would we want to teach people about money? They might start asking questions’” – Garrick Hileman

What do you think a shift toward CBDCs could look like in the next few years? Are there any big risks involved?

Garrick Hileman: I think it’s so early still, in the UK, in the US, and in Europe. We, the citizens, still have a huge say in how this could go. It’s not fated to go a particular way, it’s really an open question. What kind of money we want? What values do we want imbued in our money? What levels of privacy do we want? What levels of efficiency do we want? Do we want more control of our money? Do we want things like cash to continue to exist? This is a debate that’s going to grow, and I would argue it’s still in the early days, even though people have been talking about CBDCs for a decade.

The big risk would be that something happens too quickly, without enough input from society. I think this is where it could go really wrong, if there’s a rush to implement something without getting the public educated and involved in the discussion.

What would you say to members of the public who find it hard to take interest in CBDCs, or find it all too confusing?

Garrick Hileman: We’ve got a massive financial literacy problem that goes all the way up to the top of the socioeconomic ladder. People want money to just work, but what they don’t understand is [that] if you leave the design discussion to others, it may not wind up working very well for you. In fact, I would argue that’s very much the case today, and people are getting ripped off by the monetary system we have in place. Honestly? I’ve heard regulators say: ‘Well, why would we want to teach people about money? They might start asking questions.’ I’ve literally heard those exact words come out of a regulator’s mouth. That’s where some of these technocrats are at.

I think it’s important that people be a little patient with themselves, [even] if they don’t grasp the nuances right off the bat. It’s worthwhile, because [CBDCs] are going to have a major impact on our lives going forward, perhaps as great as artificial intelligence, and robotics, and other kind of breakthrough technologies. This is such an important technology that you cannot leave it to the technocrats to make all the decisions. It’s a political issue that has to be resolved above the technocratic layer of society. There are major implications for individual privacy and financial access, and frankly what type of world we want to live in.

Join Dazed Club and be part of our world! You get exclusive access to events, parties, festivals and our editors, as well as a free subscription to Dazed for a year. Join for £5/month today.

Author

Violeta Rojo

EDM LOVA